Howard Bluston discusses the implications of the consultation process for levelling up as it will affect pension funds, and sees...

April 17, 2023

Report

|

Written By: Chris Santer |

|

Paul Myles |

Chris Santer and Paul Myles from Schroders Capital discuss place-based impact investing and why pension fund capital is well suited to funding these investments

What is place-based impact investing?

In a nutshell place-based impact investing (PBII), seeks to deliver positive social and environmental outcomes to a place as a direct result of investment, alongside financial return. The government’s plan to “level up” the UK needs private sector support to be successful, and it’s not just about the capital needed. There are skills in the private sector that the government needs to tap into, to make a lasting and meaningful difference.

Real estate forms a central pillar of PBII, specifically seeking to deliver improved regional prosperity, employment prospects and housing quality. It seeks to do so by developing housing, workplaces and regenerating town centres. We believe PBII can address some of the drivers of social deprivation and inequality, while offering an attractive risk-adjusted return for institutional investors. It is not philanthropy.

Returns are important, as is demonstrating “additionality”, in order to attract and retain investors. Additionality means the delivery of positive impact outcomes, beyond that which would have been delivered by investors driven solely by financial profit. A robust framework to establish intent and measure this additionality is, therefore, a non-negotiable part of a successful PBII strategy.

Where and how can we create impact?

Investors with a focus on projects delivering new homes can address two challenges in one go: the shortage of new housing; and bringing life, vitality, footfall and spend back into UK town centres. Put simply, we have too many shops and not enough homes. Our focus is to have both a social impact, particularly place-based inequality, and deliver a financial return. We do this primarily, but not exclusively, by investing in deprived areas.

Last year, economic output (GDP) per head in the UK varied from £65,500 in Kensington & Chelsea (London) the wealthiest area, to £14,300 in Torbay (Devon) the poorest area. That’s a five-fold difference.

International comparisons suggest that the differences in income per capita across different parts of the UK is significantly bigger than in other advanced economies such as France, Germany, Japan and the US. It is closer to Hungary and Poland. What’s more, the gap within the UK appears to have widened over the last decade.

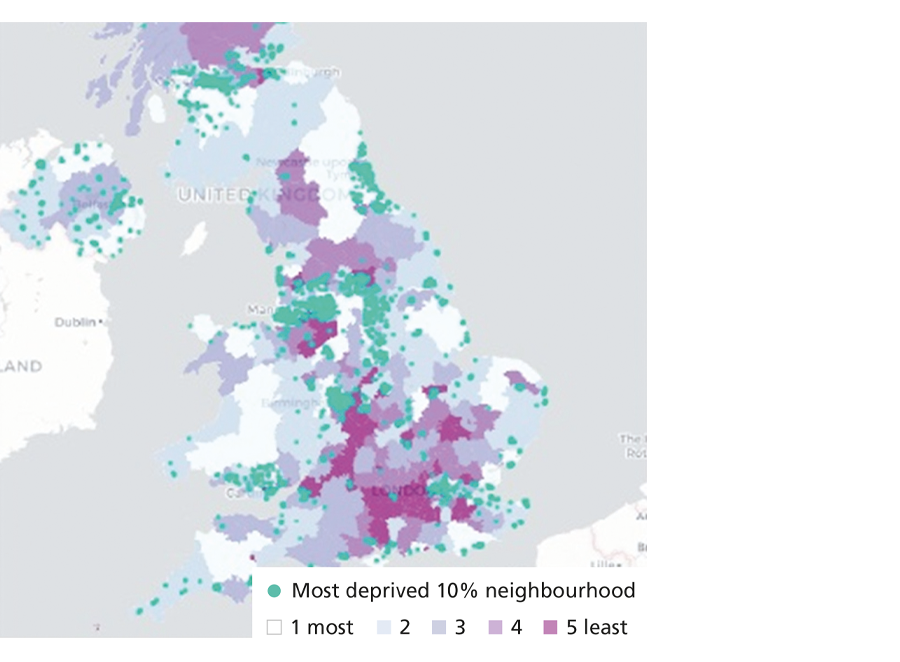

Figure 1: Deprived areas – there are pockets of deprivation across the UK

Source: ONS English (2019), Northern Ireland (2017), Wales (2019), Scotland (2020) Indicies of Deprivation. 606221

The most deprived areas – those in the bottom 10% of the ranking – are spread across the UK. There are no regional concentrations, nor is deprivation present only in inner cities. Indeed, three-fifths of local authorities have a least one neighbourhood which is among the most deprived nationally and a sixth of the most deprived areas in England are in “the South” (here defined as London, South East, South West and East of England).

How can we evidence the impact and what does success look like?

The diverse nature of real estate, and the intangible characteristics of social impact outcomes, means that investors can struggle to decipher and measure impact outcomes. It’s vital to have a consistent and reliable framework to measure impact outcomes.

Our framework uses three core attributes, implemented at both a fund- and asset-level.

Intent: Establishing what outcomes the fund investments want to deliver

Contribution: Establishing how our real estate investment will deliver the objectives

Measurement: Our team define clear metrics or key performance indicators for each project in the portfolio, with the strategy independently evaluated on an annual basis to ensure accountability and transparency for investors.

By way of a real-world example, our impact objective (intent) for a town centre regeneration might be to reduce the “empty streets” phenomenon and reinvigorate lively and inclusive town centres. Here we could measure the percentage reduction in under-utilised space by square metres, how many new homes have been provided, as well as how much public realm/green space has increased. We could gauge the percentage of retail space leased to independent businesses, as well as the number of jobs created.

These factual measures are necessary but don’t always capture the impact on peoples’ lives. As such, we would also assess the indirect benefits via surveys of residents or locals. The success of towns and communities is intrinsically linked to local people and their needs. The impact of projects beyond immediate beneficiaries – usually tenants – needs to be captured.

Finally, the standardised metrics or key performance indicators – linked to local needs at both an asset and fund level – should be shared with investors periodically. This reporting should combine quantitative and qualitative data, including stakeholder voice, to provide a holistic view of impact creation not captured by measuring metrics alone. We think annual reporting is an appropriate timeframe to demonstrate progress, recognising regeneration and social impact can take time to deliver.

Why is institutional money (pension funds) an ideal source for investing in this type of asset class?

In its “Levelling Up” white paper published in February 2022, the government recommended LGPS pooling organisations allocate 5% of portfolios to local investing.

That would equate to £16 billion allocated to new UK investments. That wealth of capital would make the Local Government Pension Scheme an important stakeholder in the delivery of tangible solutions to social issues that meet the stated requirements and future needs of communities and councils.

With PBII – targeting tangible outcomes such as jobs, housing and reducing the number of boarded-up shops in a town centre – investors can see where the money has been spent. This isn’t chasing short-term profits overseas. It is addressing a domestic housing crisis, supporting increased employment & training and revitalising empty high streets.

There is no “quick fix” solution for social deprivation. Many projects may take years to see the positive social impact. Due to a longer investment horizon and with allocations to illiquid UK investments, LGPS can meet both their fiduciary duty and financial targets alongside measurable positive impact.

PBII delivers both financial and social returns. Even so, it’s important to operate from within a clearly-defined investment and impact framework to be able to articulate intent, what will be delivered and how it will be measured. This builds trust but also demonstrates additionality – that these investments wouldn’t have been undertaken by investors driven purely by financial profit.

But these things take time – both to deliver major projects and to measure the social impact – which is why the LGPS is critical to the future success of the UK. The patient nature of its capital can achieve meaningful positive change without giving up the financial returns.

|

|

|