Eric Lambert, Actuary and Independent Investment Adviser, discusses the fundamental question of the difference between strategy and implementation and shows...

April 18, 2024

Comment

|

Written By: Thomas Sarno |

|

& Eric Cooperström |

|

& Mary Ellen Aronow |

Thomas Sarno, Eric Cooperström and Mary Ellen Aronow of Manulife provide a wide-ranging survey of recent developments in the forest-carbon market, and note what is required of timberland owners in order for them to successfully incorporate carbon values into their investment strategies

The volume of carbon credit trading has grown dramatically over the past few years. As demand surges, prices have risen, and the carbon marketplace has become more transparent – and functional. The rapid development of carbon credit markets and increasing commitments by governments and corporations to create explicit goals for greenhouse gas (GHG) emissions reduction have underlined their necessary role in global decarbonisation, supporting the anticipated upward appreciation in the price of carbon in coming decades. The development of increasingly clear and consistent standards-setting requirements for carbon credit projects together with more robust certification and verification of project results provide a foundation for investor confidence and continued growth for carbon markets.

Dramatic growth in carbon credit demand is increasing competition in timberland transactions

Forestry projects represent a major component in the present and future supply of tradeable carbon credits. The ability of forests to cost-efficiently capture and store large volumes of CO2 for the long term is increasingly recognised by timberland investors and managers who are already starting to incorporate potential carbon values into their valuation and investment strategies. Timberland’s ability to support net zero goals alongside generating financial returns is becoming an observable factor in increasing competition in timberland transactions. To effectively invest and operate in the coming decades, timberland owners will need to prioritise staying informed, engaged, and responsive to highly dynamic carbon markets.

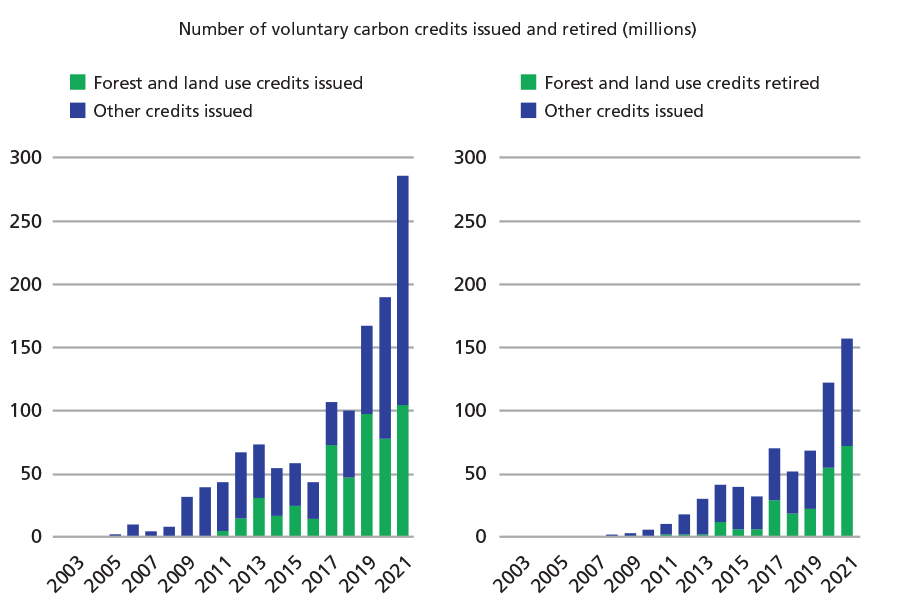

Figure 1: Accelerating growth seen in traded voluntary carbon credits

Source: Berkeley Voluntary Registry Offsets Database, Version 5, April 2022.

Between 2016 and 2021, growth in voluntary carbon credit issuance accelerated, increasing by over 300%. In 2021, 285 million carbon credits were issued, and the first quarter of 2022 alone saw the additional issuance of 79 million carbon credits. Annual demand (retirements) of carbon credits – a measure of a purchaser’s one-time use of a carbon credit to compensate for, or neutralise, emissions – has also increased rapidly, experiencing breakneck growth since 2016. In 2021, 158 million carbon credits were retired, up 28%, from 123 million in 2020. Future demand for carbon credits is forecast to grow exponentially between now and mid-century to meet corporate net zero target dates, according to a study by research company BloombergNEF, with corporations driving this steep demand growth.

Renewable energy and forestry projects dominate the current supply of tradeable carbon credits

A measure of the global voluntary carbon credit supply is the 5,000+ carbon projects registered with the four main programmes (American Carbon Registry, Climate Action Reserve, Verra, and Gold Standard), with renewable energy and forestry projects representing over half of the total projects registered to date. As of Q1 2022, over 625 individual voluntary forestry and land use carbon projects have been registered, representing a combined 556 million carbon credits, or 40% of total issued credits.¹

Three-quarters of these forestry and land use carbon credits are developed from projects classified as reducing emissions from deforestation and forest degradation (REDD+), falling into the avoided emissions category, and are located in developing countries. Given the questionable past performance of several REDD+ projects, these may face higher scrutiny in the future. Of the remaining 25% of registered forestry and land use carbon credit projects, 16% are classified as improved forest management projects, with the remaining share of projects classified as afforestation/reforestation (8%), wetland restoration (0.2%), and grassland management (1%).

Improving confidence in the quality of both carbon credits and governance

The voluntary carbon market is seeing greater investor acceptance as more specific and accessible price information becomes available. The expansion of market services specific to carbon credits is providing a foundational framework for making carbon credits comparable to other traded commodities.

This improved market infrastructure has been accompanied by an increase in disclosure and reporting standards, third-party carbon credit certification, and carbon project rating services. While the improved transparency, consistency, and verification of carbon credit trading are supporting the growth of future demand, policy and technological developments are also signalling significant changes to the future supply of carbon credits: Distinctions are being drawn between credits that represent the removal of GHGs from the atmosphere versus credits that represent emissions avoidance. Carbon policy is moving in the direction of explicitly favouring projects that generate removal credits, such as those from forest carbon sequestration or direct air capture, and placing higher hurdles on certifying avoidance projects, such as avoided deforestation (REDD+) and the use of renewable energy projects that potentially displace fossil-fuelled power plants.

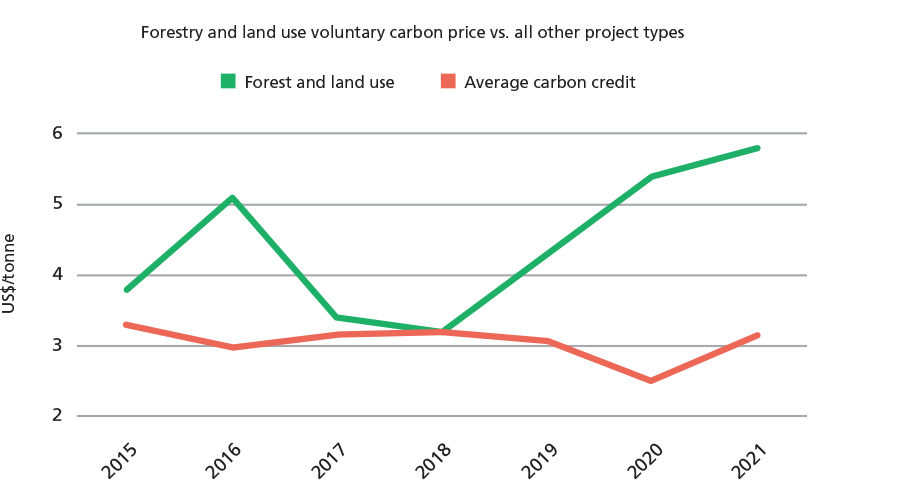

The costs of solar and wind power have dropped precipitously over the past decade and are now competitive with fossil fuel power in most developed economies, diminishing the rationale for their use in generating carbon credits. In the future, the use of renewable energy projects for the issuance of carbon credits will likely be limited to emerging economies, particularly in Africa, where carbon finance can support project feasibility. Since REDD+ and renewable energy have been large components of the overall supply of carbon credits, new restrictions on these types of projects will likely shift demand to high-quality forest projects and other new classes of carbon credit projects. Markets are becoming more cognisant of the differences in quality arising from various project types and are assigning price premiums to higher-rated projects such as forest carbon sequestration.

Figure 2: Carbon credit prices recognise forestry projects as a premium removal

Source: “State of the Voluntary Carbon Markets 2021, Installment 1,” Forest Trends, September 15, 2021; Manulife Investment Management research, as of August 2022.

Carbon moves from incidental to core consideration within timberland investment

Whether or not a particular timberland property is better suited primarily for commercial timber production or for carbon sequestration depends on an investor’s goals and priorities, and the decision will also be heavily influenced by assumptions around the development of carbon policy and the future trajectory of carbon and timber values.

Timberland investors and managers have started to incorporate potential carbon values into their valuations and investment strategies: The inclusion of carbon values in the investment calculus of properties in certain regions with lower traditional stumpage values is suspected to have contributed to strikingly robust transaction prices in some recent timberland sales. For example, a large timberland property in the US lake states, with no differentiating attributes from other properties in the region, traded for an implied purchase price of US$1,017 per acre² in 2021, compared with the regional five-year average price of US$636 per acre, a value that until now has varied little over the past five years.³ Manulife Investment Management’s 2021 purchase of 90,000 acres of Maine timberland included the commitment to build carbon inventory to progress the company’s climate action plan. And IKEA has secured 1.3 million acres in the US South over the past four years with the stated intent of using the properties to meet corporate carbon net zero goals.

With prices for carbon credits expected to rise, the economic rationale for carbon-focused investment in timberland will improve, enabling investors with carbon-oriented objectives to be increasingly competitive with those focused on commercial timber production. Currently, carbon-focused US timberland investors are more competitive in regions with significant timber resources but less concentrated commercial demand, and as the relative price of carbon credits converges with the values generated by a particular region’s timber production, stumpage prices in that region could be pushed higher to motivate landowners to continue to produce timber for in-place forest product facilities. Lumber, wood panels, and other forest product mills may also need to adapt to changes in timber supply due to a shift to more carbon-oriented timberland management regimes, as well as to changes in demand tied to a shift away from concrete and steel construction to wood-based building systems with a much lower carbon profile.

With the growing commitment to carbon-focused management by different types of private timberland owners, regional timber availability may become more constrained and could result in forest product companies adapting raw material sourcing strategies to increase security of supply. Mills could increase acquisitions and direct management of nearby, or logistically feasible, timberlands and more actively engage with large, neighbouring timberland owners in formal, long-term supply agreements.

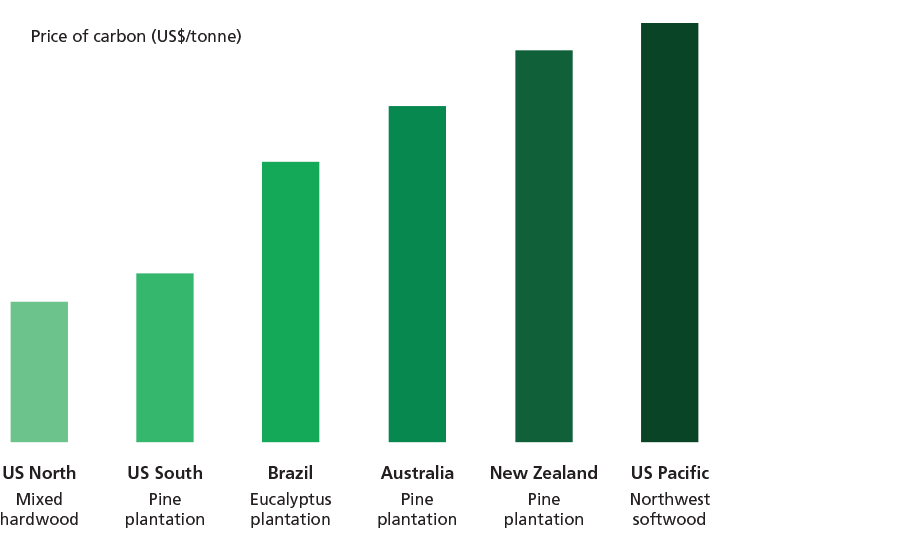

Timberland owners are likely to demand higher carbon prices to compensate for delayed harvesting

In core timberland supply regions such as the US South or Pacific Northwest, our research estimates that carbon credit prices for forest carbon removal projects would need to rise from recent average levels of US$7 per tonne to motivate timberland owners to accept a long-term delay in harvesting in favour of accumulating carbon stocks on their properties. If the price of forest carbon credits were to reach an average of US$30 per tonne, potential carbon returns would approach parity with current expected returns for traditional timber production management on a US southern pine plantation.

Figure 3: Carbon prices necessary to shift from traditional timberland investment management vary

Source: Manulife Investment Management research, July 2022. Break-even prices represent the level of carbon price at which carbon projects yield returns equivalent to timber production-focused management.

Many aspects of the forest carbon market are still actively in development, but timberland owners will need to build out their resources to stay current, engaged, and capable of responding to markets and policy developments if they’re to successfully incorporate carbon values into their investment strategy and on-the-ground management plans. Areas adding risk and requiring a keen focus include evolving quality and integrity standards, and governance to meet carbon additionality requirements.

Timberland markets are already adapting to new patterns of investing and managing timberland to account for carbon values. And incorporating carbon values into the timberland investment process and property management plans provides greater optionality for reaching a range of financial and environmental goals. Meanwhile, the rapid growth of new wood-based building systems for multistorey buildings is creating a significant extension to the long-term storage capacity of CO2 captured by forests in the built environment. Depending on how this new layer of carbon sequestration is incorporated into global net zero accounting, the dividing line between the management of timberlands for carbon sequestration, as opposed to timber production, may become more blurred. This further supports timberland owners retaining optionality in their longer-term management planning, and the explicit inclusion of carbon values into all aspects of the timberland investment process builds on well-established sustainable management practices that are the bedrock of the timberland asset class.

In the UK: Issued and approved by Manulife Investment Management (Europe) Limited. Registered in England No.02831891. Registered Office: One London Wall, London EC2Y 5EA.

Authorised and regulated by the Financial Conduct Authority. In the EEA: Issued and approved by Manulife Investment Management (Ireland) Limited. Registered office located Second Floor, 5 Earlsfort Terrace, Dublin 2, D02 CK83, Ireland.

1. Berkeley Voluntary Registry Offsets Database, Version 5, April 2022 ; Manulife Investment Management research, as of August 2022

2. “Timberland Markets Report,” Fastmarkets RISI, April 7, 2022.

3. NCREIF Timberland Index, as of Q4 2021.

Published: April 19, 2023

Home »

Climate Change